Two New Uncorrelated Strategies Added to High Sharpe Portfolios

February 26, 2026

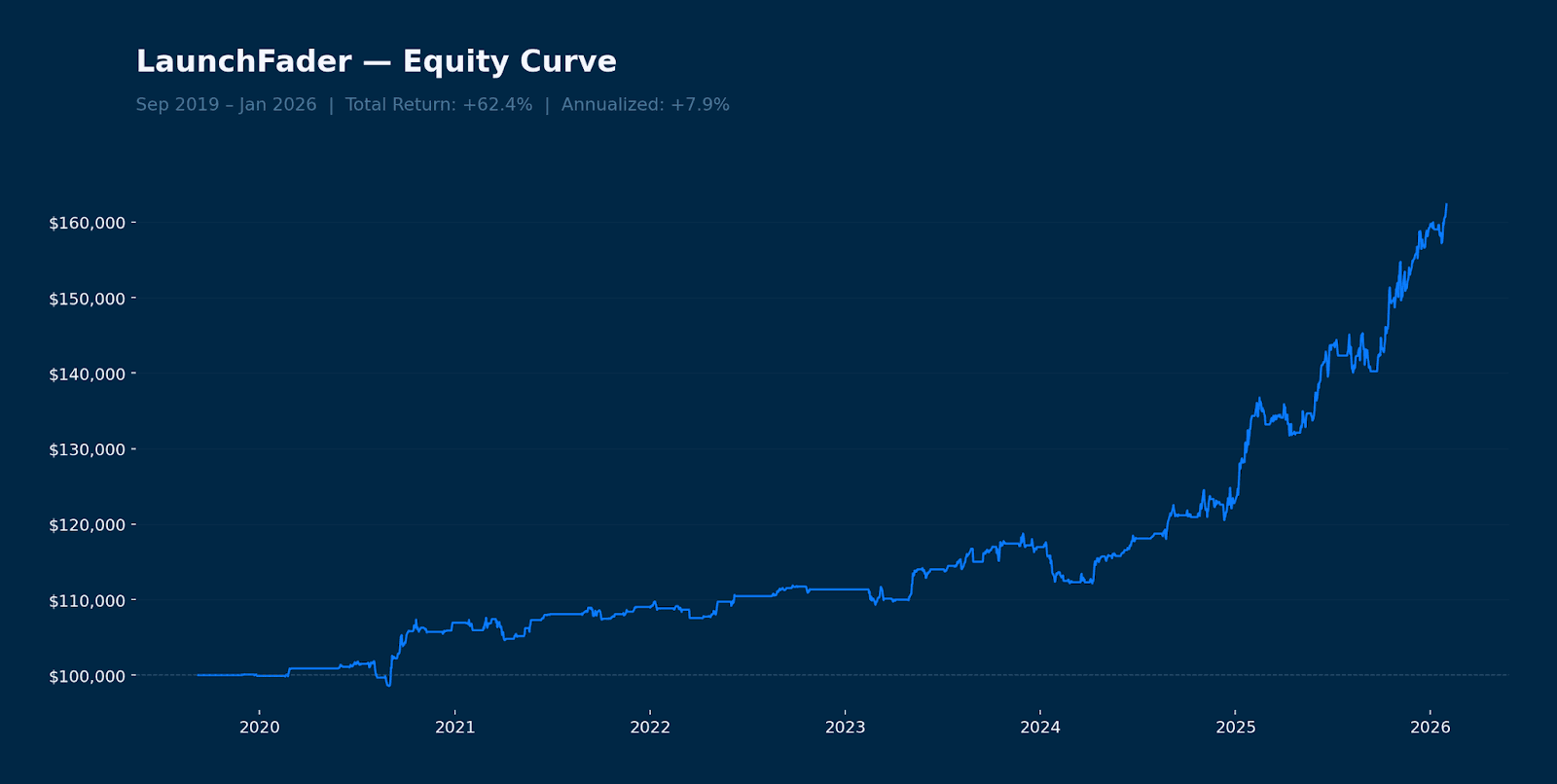

Launch Fader

This strategy structurally shorts low-quality projects during their initial exchange onboarding phase. By identifying and fading weak launches early, we capture value from the natural price decay that follows hype-driven pumps.

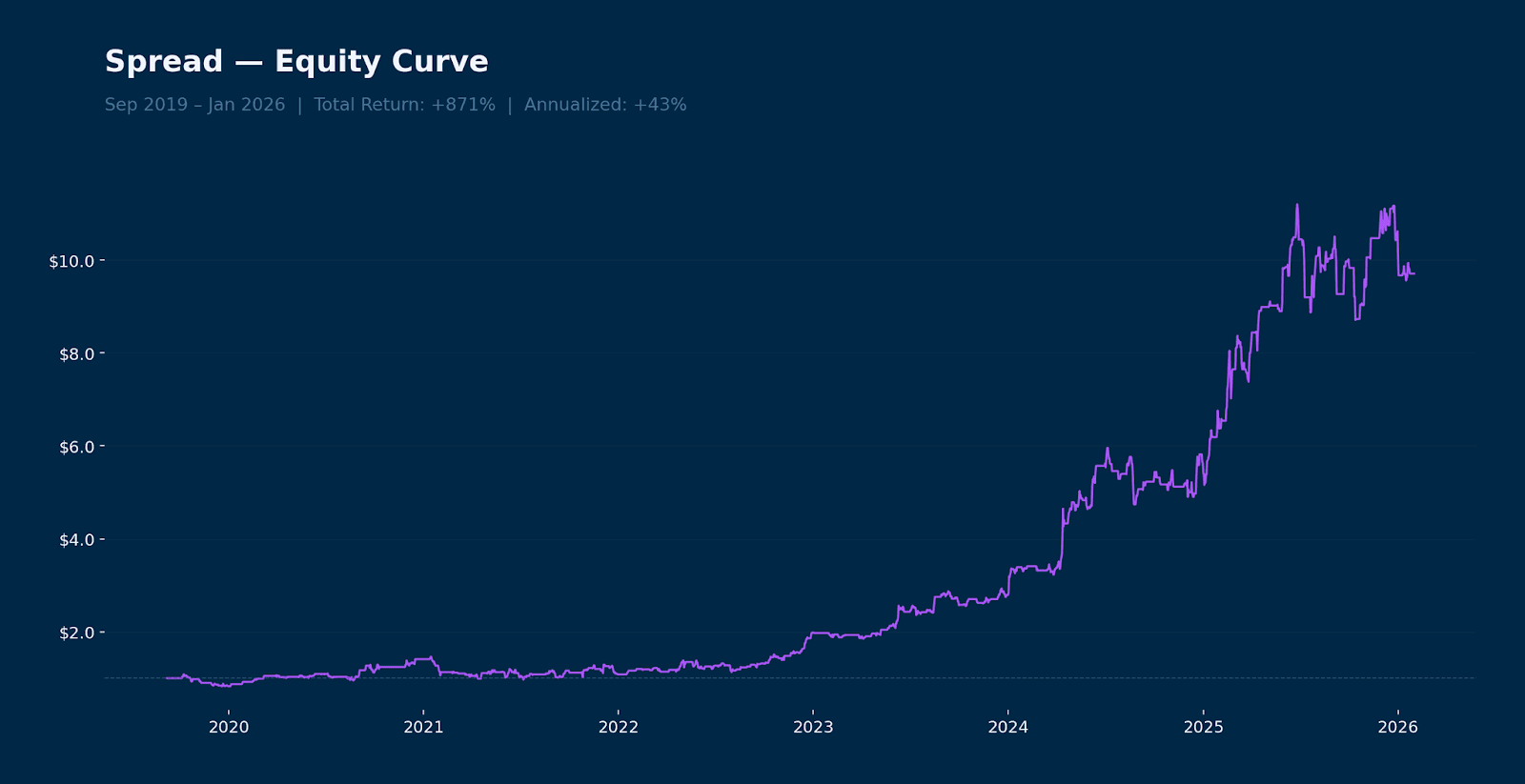

Spread Long & Short

This strategy trades relative momentum within the crypto market. It shorts underperforming coins while hedging with positions in larger, high-volume assets. The approach captures alpha from market dispersion while maintaining overall portfolio stability.

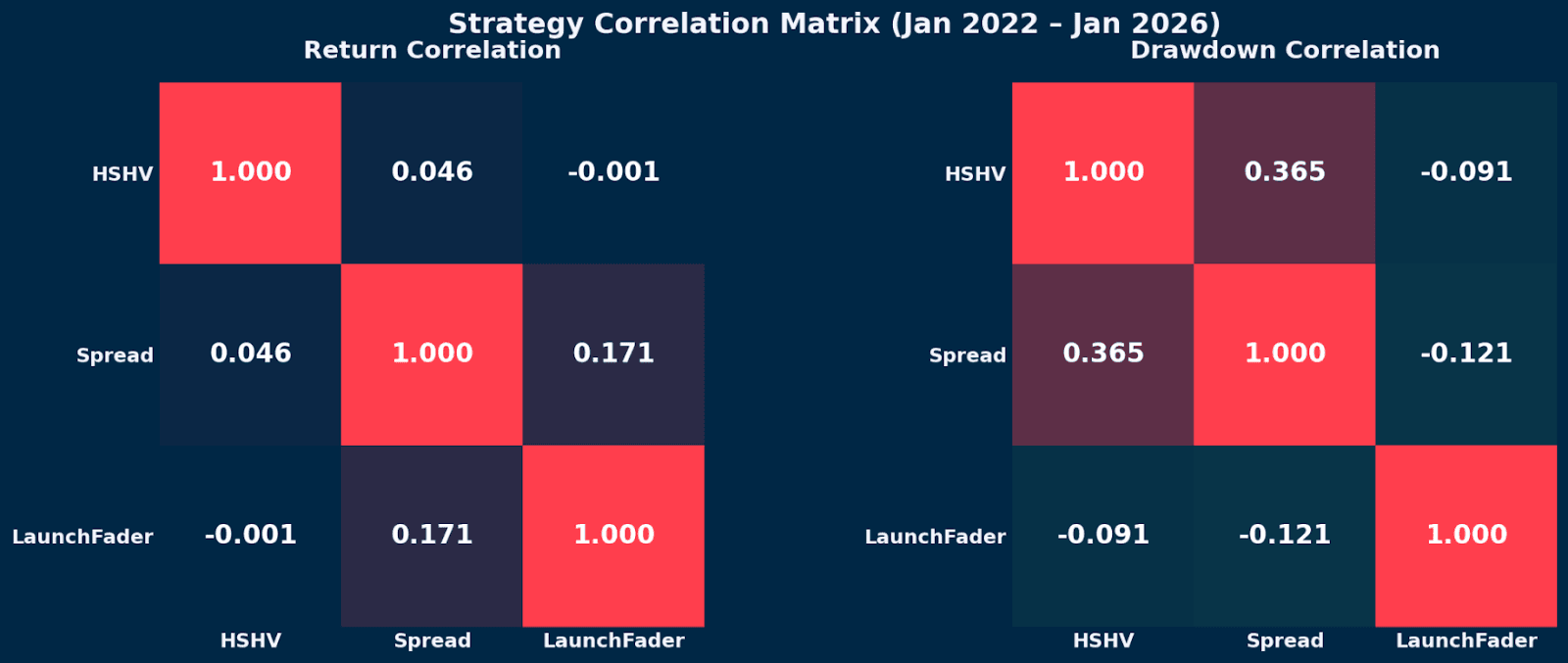

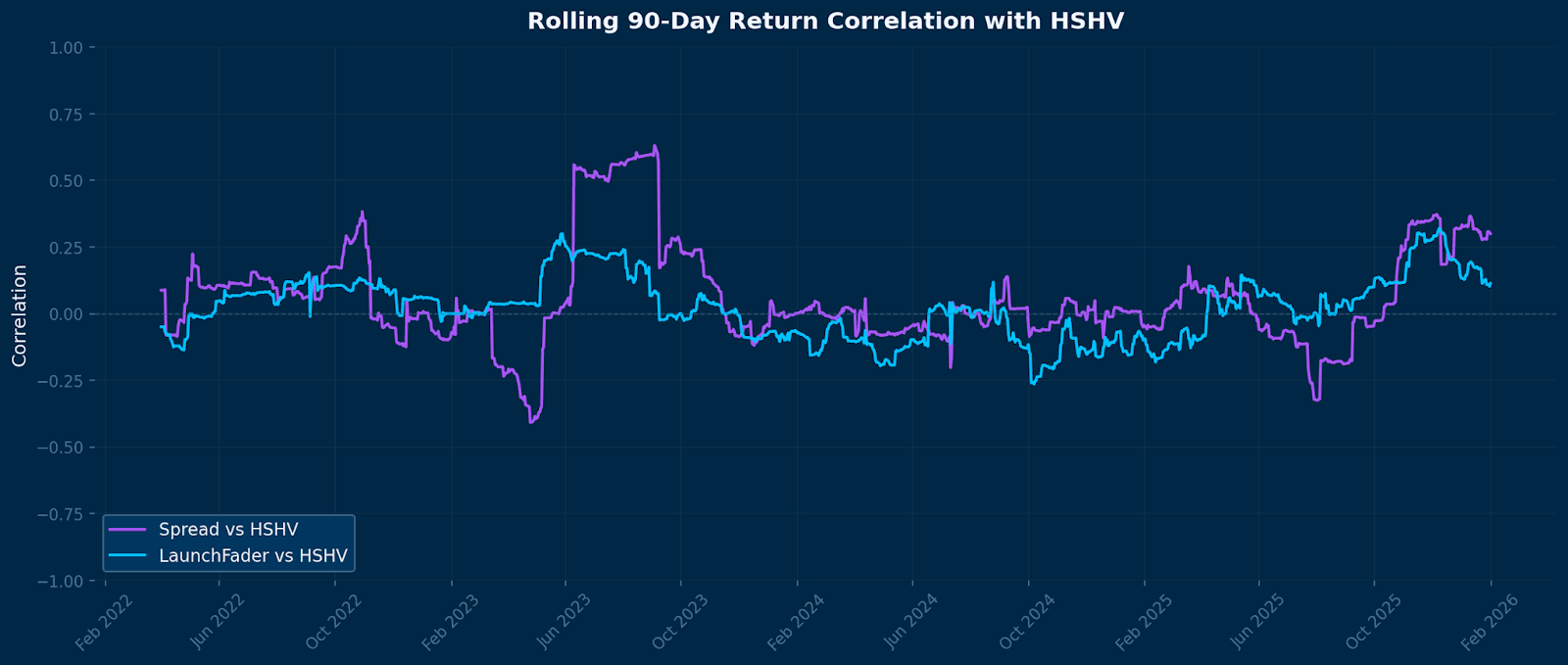

Portfolio Correlation

Both strategies add uncorrelated returns to our existing portfolio. Launch Fader capitalizes on behavioral inefficiencies in new listings, while Spread Long & Short extracts value from relative strength dynamics across the market. Below you can see their relative correlation to the portfolio on a 90-day rolling basis.

A correlation near 0 means the strategy moves independently of the portfolio. Near +1 means they move together; near -1 means they move in opposite directions.

Our research is primarily focused on models that exhibit low drawdown correlation with the total portfolio: